Production

Principles of production

In order to produce goods and services which can be sold, and generate revenue and profits, a firm must purchase or hire scarce inputs, which are its factors of production. These factors can be fixed or variable.

Fixed factor inputs

Fixed factors are those that do not change as output is increased or decreased, and typically include premises such as its offices and factories, and capital equipment such as machinery and computer systems.

Variable factor inputs

Variable factors are those that do change with output, which means more are employed when production increases, and less when production decreases. Typical variable factors include labour, energy, and raw materials directly used in production.

Time periods for the firm

The fundamental principles of production relate closely to the time periods in question, of which there are four:

The very short run

A firm is said to be in its very short run when the only way to increase output is by using up existing stocks of inputs.

The short run

A firm is said to be in its short run when it can increase its output by using more variable factors, such as by hiring more workers, but not by increasing its fixed factors. In the short run firms do not use extra fixed factors, such moving to new premises, to increase output. Therefore, in the short run at least one factor of production is fixed.

The long run

A firm enters its long run when it increases its scale of operations. Increasing scale means that no factor of production is fixed, and all are variable. Typically, this means that a firm expands by building or renting larger premises, purchasing or leasing new machinery and employing more workers.

The very long run

A whole industry enters the very long run when there is a significant change in the use of technology. For example, the widespread use of the internet to book holidays has drastically altered how the holiday industry is structured.

Economic analysis tends to focus only on the short and long run, and largely ignores the very short and very long run.

Time periods for a market

A whole market can also be considered in terms of the short and long run.

The industry short run

An industry is in its short run when its capacity is fixed. This usually means that the number of firms in the industry is fixed, with no new firms entering or leaving the market.

The long run

This exists when there is an increase, or decrease, in the capacity of the industry to produce, and this usually means that the number of firms in a given market increases, or decreases.

The law of diminishing returns

The law of diminishing marginal returns comes into play whenever a firm tries to increase output by applying additional variable inputs to a fixed factor. Production requires the combination of both fixed and variable factors to create an output. Economic theory predicts that if firms increase the number of variable factors they use, such as labour, while keeping one factor fixed, such as machinery, the extra output or returns from each additional, marginal unit of the variable factor must eventually diminish.

Diminishing marginal returns forms part of a larger principle, called the principle of variable proportions. This states that, assuming one factor is fixed, the marginal returns generated from adding new variable factors will not be constant. In fact, returns will rise at first, reach a turning point, and then eventually diminish. The law of diminishing marginal returns simply refers to the last phase of this wider principle.

Consider the following example:

Returns to labour

Assuming one factor is fixed, the addition of extra workers will result in increasing returns followed eventually by diminishing returns.

| WORKERS | TOTAL PRODUCT | AVERAGE PRODUCT | MARGINAL PRODUCT |

| 1 | 6 | ||

| 2 | 16 | ||

| 3 | 28 | ||

| 4 | 42 | ||

| 5 | 56 | ||

| 6 | 66 | ||

| 7 | 69 | ||

| 8 | 70 | ||

| 9 | 69 |

Exercise

Consider the total output produced by workers making hand-crafted wooden cabinets, and calculate:

- Average product, which is output per worker

- Marginal product, which is the additional output from adding one extra worker.

Observations

What happens to productivity?

Marginal productivity is relatively low when only a few workers are employed. However, marginal productivity rises quickly as each extra worker contributes more than the previous one. Eventually marginal productivity begins to decline, in this case, with the employment of the fourth worker. With the employment of seven workers marginal product is zero, and total product is at a maximum. This means that marginal productivity is low at the extremes of output – at high and low levels.

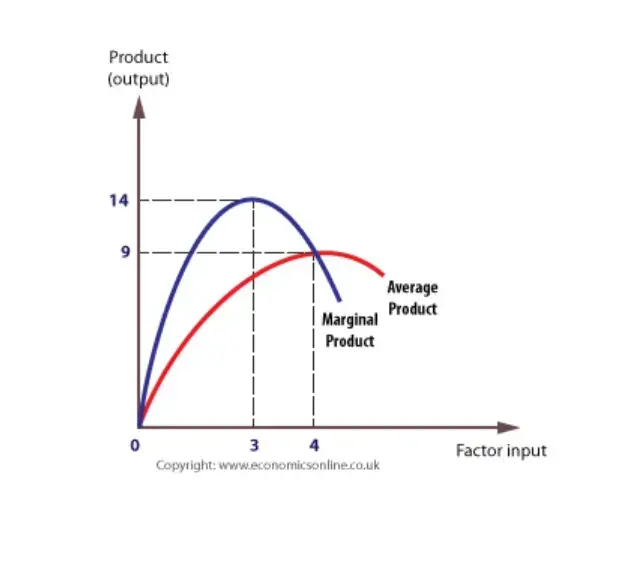

Product curves

It can be observed that, at first, the marginal returns curve increases and then decreases. The marginal returns curve cuts the average returns curve when average returns are at their peak.

How is this pattern explained?

With a small number of workers, output is low and a division of labour cannot be employed, and workers cannot specialise or develop new skills.

However, marginal returns increase quickly as specialisation occurs and efficiency increases. This creates the opportunity for labour to develop skills and become more productive.

Eventually, marginal returns diminish as the effects of specialisation and new skills wear off. This pattern has a considerable impact on the firm’s short-run cost curves.