Marginal cost

Marginal cost – definition

Marginal cost is the additional cost incurred in the production of one more unit of a good or service. It is derived from the variable cost of production, given that fixed costs do not change as output changes, hence no additional fixed cost is incurred in producing another unit of a good or service once production has already started.

Example

| Output | Total cost (£) | Marginal cost (£) |

| 10 | 400 | |

| 11 | 700 | 300 |

| 12 | 800 | 100 |

| 13 | 1000 | 200 |

| 14 | 1500 | 500 |

Marginal cost will tend to fall at first, but quickly rise as marginal returns to the variable factor inputs will start to diminish, which makes the marginal factors more expensive to employ. This is referred to as the ‘law of diminishing marginal returns’.

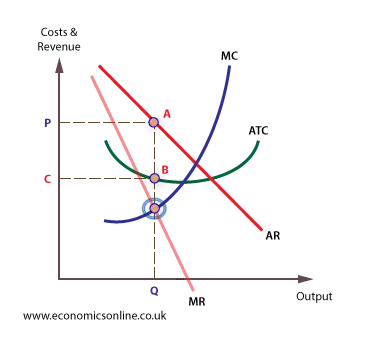

Marginal cost is significant in economic theory because a profit maximising firm will produce up to the point where marginal cost (MC) equals marginal revenue (MR).

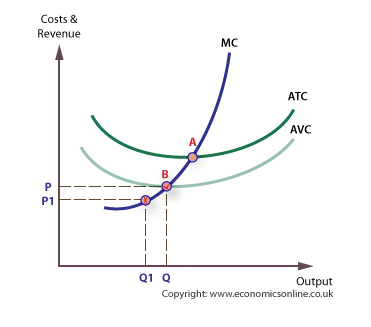

Also, a firm’s supply curve is effectively the part of the MC curve above average variable costs (from point B upwards, on the diagram below). A firm will not supply below this point as it will not be covering its opportunity cost. Point B is also known as shut-down point. Point A represents break-even point.

-

Read more on profit maximisation